Learn how to coordinate your retirement accounts like an orchestra to help maximize your retirement strategy.

Key Takeaways

- Understanding the retirement savings hierarchy can help maximize your limited dollars. Many financial professionals suggest prioritizing your 401(k) first, then your Traditional IRA, and finally, your taxable savings when determining how to allocate retirement funds.

- Coordinating investments across accounts may enhance your overall strategy. Some approaches involve placing income-generating assets like bonds in tax-deferred accounts while using taxable accounts for growth-focused investments like stocks.

- Your withdrawal strategy can impact your retirement income. Options include tapping taxable accounts first, withdrawing from poor performers, or using a tax-bracket approach, each with different potential benefits depending on your circumstances.

An orchestra is merely a collection of instruments, each creating a unique sound. It is only when a conductor leads them that they produce the beautiful music imagined by the composer.

The same can be said about your retirement strategy.

The typical retirement strategy is built on the pillars of your 401(k) plan, your Traditional IRA, and taxable savings. Getting the instruments of your retirement to work in concert has the potential to help you realize the retirement you imagine.1

Hierarchy of Savings

Maximizing the effectiveness of your retirement strategy begins with understanding the hierarchy of savings.

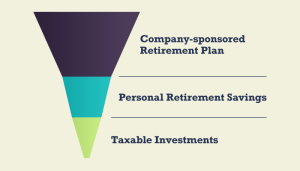

If you’re like most Americans, the amount you can save for retirement is not unlimited. Consequently, you may want to make sure that your savings are directed to the highest-priority retirement funding options first. For many, that hierarchy begins with the 401(k), is followed by a Traditional IRA, and, after that, extra money is put toward taxable savings.

You will then want to consider how to invest in each of these savings pools. One strategy is to simply mirror your desired asset allocation in all retirement accounts.2

Another approach is to put the income-generating portion of the allocation, such as bonds, into tax-deferred accounts while using taxable accounts to invest in assets whose gains come from capital appreciation, like stocks.3

Withdrawal Strategy

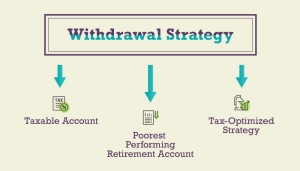

When it comes to living off your savings, you’ll want to coordinate your withdrawals. One school of thought recommends that you tap your taxable accounts first so that your tax-deferred savings will be afforded more time for potential growth.

Another school of thought suggests taking distributions first from your poorer-performing retirement accounts since this money is not working as hard for you.

Finally, because many individuals have both traditional and Roth IRA accounts, your expectations about future tax rates may affect what account you withdraw from first. (If you think tax rates are going higher, then you might want to withdraw from the traditional before the Roth). If you’re uncertain, you may want to consider withdrawing from the traditional up to the lowest tax bracket and then withdrawing from the Roth after that.4

In any case, each person’s circumstances are unique, and any strategy ought to reflect your particular risk tolerance, time horizon, and goals.